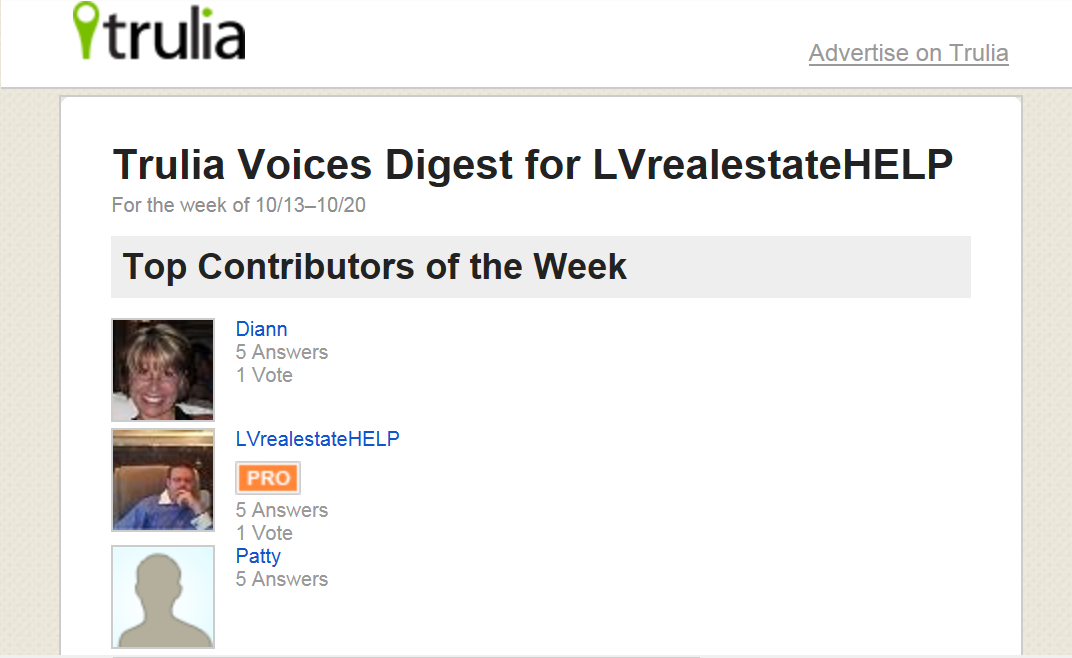

If you are asking yourself "Why is the market going to soften in Las Vegas in 2014??" You should read this article: Buying right now?? Make sure you BUY SMART, so you don't REGRET it in 2014! If you are short selling the Debt Relief Act is set to expire at the end of 2013. Some buyer's are still paying above appraisal value. You should sell now while you can get top dollar. As explained in the article above, inventory is on the rise and the days of 30% annual appreciation will soon be gone. Please watch the video to the left about how we can market your property and get you maximum exposure for your listing. If you have any questions about selling your home please fill out our Seller's Form HERE or feel free to contact me directly at the contact info provide below. Let the Adams Team at Rothwell Gornt Companies show you why we are the hardest working agent in town. Best Regards, We made the Top Contributor's List for Trulia again last week for 10/13/2013 to 10/20/201310/21/2013  Best Regards,  I bought my first RE property on 6/2/2002 when I was 21. I had saved money from various jobs and from a couple cars that I had sold for a profit. It was a 2 story condo with 1,424 sqft, 2 bedrooms, 2.5 bath, and a 1 car garage. I bought it for $107k. I rehabbed it from top to bottom. Granite counters in kitchen, and bathrooms. New carpet and tile flooring with black marble borders and baseboards, new paint throughout, new window coverings, new light fixtures throughout, mirrored walls, new sinks and faucets, and new appliances throughout. Amazingly I did all that for around $20k. It was good to have good friends help with the rehab/rehab costs. I lived in this unit for a while so I wanted it to be nicely upgraded. I sold it for $189k on 9/22/2004. Below are some pics of the property from an older listing but I did all of the upgrades you see except for the black cabinet doors I did not do that nor do I like it. They were all white when I was there. The dark cabinet doors make the kitchen look too dark in my opinion. It already has black appliances, sink, and dark counters so the dark cabinet doors are over kill. I saw that the current owner bought it as a foreclosure for 50k in 2011. What a steal! Maybe I will buy it back again.... Best Regards,  "With inventory rising and the market setting itself up to soften in 2014, brand new homes are looking to take it on the chin again. If you are going to buy right now, BUY SMART!" ~ Robert Adams Broker/Salesman and Team Leader of The Adams Team at Rothwell Gornt Companies Supply Side of the Las Vegas Real Estate Market New homes are only being built right now because the market had an artificially low amount of homes for sale (available inventory). Over the past 2 years now you have heard people talking about their homes appreciating 30% a year! These are crazy numbers we have not heard since the bubble era. This artificial shortage was caused by AB284 which is an assembly bill that went into affect Oct 1, 2011. Prior to Oct 1, 2011 we were still in a buyer's market and we had about 14,000 homes for sale with about 5,000 REO's (foreclosures) hitting the market each month. After Oct 1, 2011 we started seeing a major decrease in foreclosures with only about 500 REO's hitting the market each month. With more regulations and potential fines hanging over the bank/lien holders' heads they opt to stop foreclosing. This changed the market and the inventory began to decrease month after month. In early 2013 we reach the 3,000 mark of available homes for sale and were in a HOT seller's market. With homes becoming so hard to find and bidding wars running up prices, new home builders began to jump in and slap up new neighborhoods again. The problem here is that they are adding to the supply side of the market because the inventory is so low, BUT the inventory is not low because of a free market with free supply and demand. It is ARTIFICIALLY low because of laws like AB284. Legislators amended AB284 by changing the "personal knowledge" clause in AB300. This should have allowed banks to start foreclosing again but at the same time they amended AB300 they amended SB321 "The Homeowner Bill of Rights". This change that went into affect Oct 1, 2013 (a few weeks ago). This SB321 set up new hurdles for banks to jump over in order to foreclose on the property so we are not expecting foreclosures to really increase in Vegas until later in the year in 2014. However, Sept 2013 had a spike of NOD's (Notice of Defaults which is the beginning of the foreclosure process) filed prior to the Oct 1st deadline. SB321 also has a big change in regards to short sales. Before Oct 1st, 2013 banks would require the short seller and buyer to sign an "Arm's Length Transaction" disclosure. This was to ensure the bank that the seller was not short selling the home to a friend or family member that was going to let them rent it back or buy it back. SB321 has now made it illegal to require an "Arm's Length Transaction" disclosure, so now people can short sell their home to a family member or friend. (the bank still has to "Approve" the short sale though). Hopefully, this helps some of the default homeowners. Another notable statistic is that even though the REO's stopped hitting the market after AB284, it doesn't mean that the home owners are not in default. We have over 80,000+ home owners in default that are not paying their mortgage and we have about 40,000 homes that are vacant. Eventually, these homes will hit the market one way or another. And when they do it will drastically increase the supply side of the market. Since April of 2013 inventory has been on the rise week after week because of the decrease in demand explained below. We are now around 8,000 available homes for sale and we are on track to hit 10,000 by the end of the year. If this happens (which I am fully confident it will) we will then see the market shift from a seller's market to a buyer's market in 2014. Demand Side of the Las Vegas Real Estate Market Demand at that time was also VERY high due to hedge funds that moved into Vegas and started buying up everything they could get there hands on with cash. Often times paying above appraisal value and out bidding the little investors and owner occupant buyers. Hedge funds were interested in the great CAP rates these rental properties would provide. You could easily get 12% on your money annually AFTER expenses. Now that prices have risen and these CAP rates have dropped to around 5% the hedge funds are either holding the rentals they have for long term cash flow and no longer buying new rentals or they are realizing their properties have gone up around 30+% and are cashing out their profits and adding to the supply side of the market. This has in turn caused demand to decrease and at the same time added to the supply side. In 2014, if the market shifts to a buyer's market you will see more homes than buyers and at that time buyers will begin to low ball again. When that happens you will see desperate sellers accepting these low offers which will in turn lower home values. Since you can buy more sqft for your money in a resale right now vs a new home, when the resale values drops it will force the new home prices to drop in order to remain competitive. For example if you pay $200k for a resale, that same home brand new will be priced around $220k. If the resale values drop to $180k no one will buy the new home for $220k so the builder must drop their prices to compete. AND the buyers that bought the home for $220k can now only resell for $180k. You can already start to see the home builders beginning to squirm as they are now offering -$15k towards down payment - Builder will pay your closing costs -Special low rates if you use their lender etc. Keep any eye out for price reductions on new home communities soon! People are not going to be very happy when their neighbor buys the same home for thousands less. It happened before when the market crashed and it will happen again. I am not saying the market is going to crash but it is going to soften. What should I do if I want to buy NOW? BUY SMART! This is the best advice we can give any buyers right now. I am not saying you should not buy right now. In fact, I have a SFR in escrow right now that I am buying. BUT you have to buy smart. Account for the market to soften. DO NOT be a buyer that is saying to themselves, "Prices went up 30% last year. It will go up 30% in 2014 too." Because it won't. Do not over pay for a property. If you can find a good deal under appraisal value then jump on it! But don't pay over appraisal value and then regret it next year. If you can be patient there are good deals to be had still. As you wait better deals will present themselves as the market softens. I would go after resales that do not have any offers on them and offer less than the comparables. Most people do not realize the market is softening yet so you will have to submit several offers to get one accepted below appraisal value but some listings are sitting and dropping their list price. Those are the properties you want to go after. Thank you for taking time to read our October 17, 2013 market update. We hope it was helpful and informative. If you would like The Adams Team at Rothwell Gornt Companies to help navigate you through this ever changing market please fill out our Buyer's Form HERE or our Seller's Form HERE. Best Regards, by Ryan Smith | Oct 11, 2013 "A bipartisan group of 66 members of the House of Representatives has signed a letter to the head of the Federal Housing Finance Agency questioning the agency’s ability to lower maximum loan amounts for Fannie Mae and Freddie Mac. The maximum limit for loans backed by Fannie and Freddie is currently $417,000 in much of the country, but ranges up to $625,500 in more expensive areas. FHFA announced last month that it was considering a reduction in the size of the loans that could be backed by the mortgage giants, which were placed under the agency’s conservatorship in 2008 after nearly collapsing in the financial meltdown." Read the full article HERE Best Regards,  Best Regards, By Lew Sichelman October 13, 2013, 5:00 a.m. Anyone thinking of skating on mortgages owned by either Fannie Mae or Freddie Mac may want to think again. As a result of new government reports, the two companies say they are going to do a better job of going after so-called strategic defaulters. Fannie and Freddie can pursue judgments against borrowers who walk away from their loans even though they have the ability to make their payments. That's called a strategic default, and many borrowers are taking that step — typically throwing in the towel because their homes are no longer worth as much as they owe. But when their homes are sold at foreclosure and the proceeds are not enough to cover their outstanding loan balances, it creates a deficiency for which many defaulters either don't realize they are liable or don't care. To date, the two government-sponsored enterprises, which are now highly profitable after five years of running in the red, haven't done a particularly good job at pursuing deficiency judgments, according to scathing reports from the Office of the Inspector General at the Federal Housing Finance Agency. But the FHFA says it is going to make the GSEs clean up their acts. And that should serve as fair warning to those who can pay but fail to do so. As the inspector general's office says time and again in the reports, chasing down strategic defaulters can not only cut the enterprises' losses on bad loans but can also "serve as a deterrent to those who would chose to strategically default on their mortgage obligations." Going after strategic defaulters is big money. According to the report by the inspector general's office criticizing Freddie Mac's lax practices, the company has left billions on the table. The report found that Freddie Mac, which has received some $71 billion in taxpayer assistance since it was taken into conservatorship by the FHFA in September 2008, did not refer nearly 58,000 foreclosures with estimated deficiencies of some $4.6 billion for collection by its vendors. Of course, only a percentage of that amount might have been recoverable because some borrowers are simply tapped out. But because the bad loans weren't even considered for recovery, Freddie Mac "eliminated any possibility" for collecting what is owed, the report said. Now extrapolate that to Freddie Mac's entire holdings and you can see we're talking some really big money here. As of December, the big secondary mortgage market company had nearly 50,000 foreclosures still on its books, carrying a value of some $4.3 billion. And as of March 31, it held 364,000 mortgages that were 60 days or more delinquent and were, therefore, likely foreclosure candidates. Fannie Mae's portfolio of troubled assets is much larger. At the end of last year, it owned more than 105,000 foreclosed properties valued at $9.5 billion and carried a "substantial" shadow inventory of 576,000 seriously delinquent mortgages that were 90 days late or more and likely to end up in foreclosure. It does a better job than the smaller Freddie Mac, according to the inspector general's office. But in a separate report, Fannie Mae earned a slap on the wrist for not taking any action on nearly 30,000 accounts because statutes of limitation had expired or were about to. For the same reason, the report says, it failed to pursue deficiencies of some 15,000 accounts that already had been reviewed for collection by its vendors. Several factors influence the decision to pursue deficiency recoveries. But most important, state laws dictate timelines for filing claims. Some states do not allow deficiency judgments at all, but they are fair game in more than 30 states and the District of Columbia. But 10 have short windows — only 30 to 180 days in which collections are allowed. But not going after defaulters where it is permissible to do so not only reduces the chances of recovering potentially billions, the reports point out, it "incentivizes" other borrowers to walk away from mortgages they can afford to pay. The new inspector general reports are a follow-up to one issued a year ago that called the FHFA, the agency that oversees Fannie and Freddie, on the carpet for failing to provide enough guidance about effectively pursuing and collecting deficiency judgments wherever and whenever possible. In September, in response to a draft of these latest reports, the agency set down requirements for both enterprises to maintain formal policies and procedures for managing their deficiency collection processes, establish a set of controls to monitor their collection vendors and comply with state laws in an effort to preserve their ability to pursue collections. And by the first of the year, the FHFA said it will begin to more closely monitor the effectiveness of Fannie Mae and Freddie Mac's deficiency judgment processes. That's government-speak for "We'll be watching you from now on, so you'd better get your collection house in order." READ THE FULL ARTICLE HERE Best Regards, Best Regards, WE JUST RECEIVED THE KEYS TO THIS NEW LISTINGS! STAY TUNED FOR NEW PICS , THEY ARE COMING! Best Regards, Trulia put out an article today that listed the Top 20 markets that have begun to see List Price Slowdowns. Our Las Vegas market was #1 on the list. What does this mean? It is confirming what we have been saying for months, "Our inventory is rising fast and no end in site. We are on track to hit 10,000 available listings by the end of the year and is up from only 3,000 available listings in April 2013." Se the full article and Top 20 List here: You can see an article I wrote in August about the market softening here: If you would like to discuss how to sell your home while you can still get top dollar before the market softens further please visit our selling real estate page here: If you are looking to buy real estate right now and want an experienced agent that can show you how to buy smart and calculate for the market softening so you are not over paying for a property then get started on our buying real estate page here: Let us show you why The Adams Team at Rothwell Gornt Companies is the hardest working real estate team in Las Vegas! Best Regards, |

Blog Author:

|